Warning: this is going to be a long, wordy post.

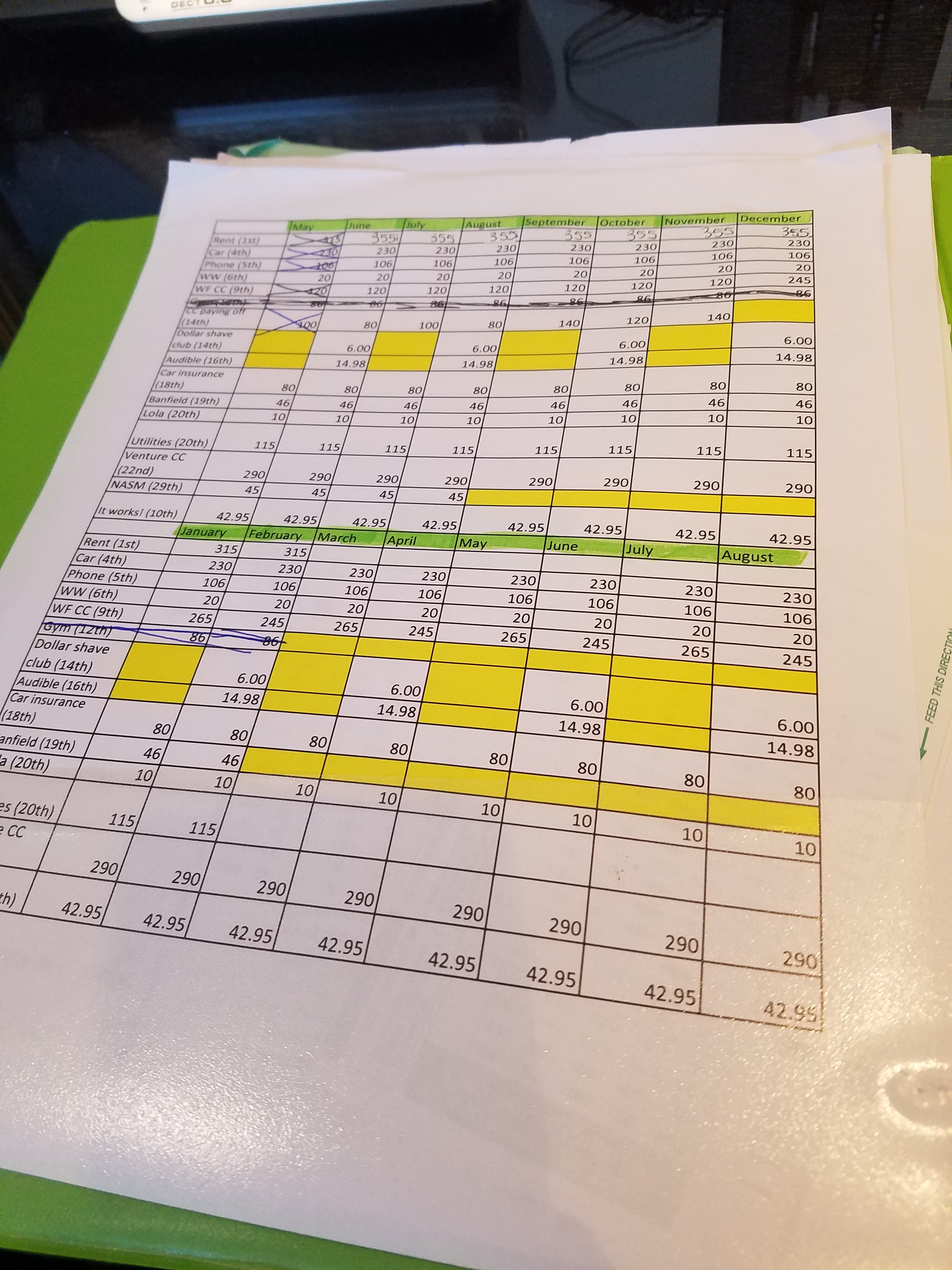

Hi!!! I have mentioned on several occasions how broke I am and one of the main reasons for that is…….my stunning credit card debt. I will go into more detail in a minute but here are some staggering things I have been realizing lately……I have not had a zero balance on a credit card since I first got one at 18. That is 11 years!!! I have been in debt for more than a decade!!!!!!!!!! I also pay $500/month in credit card bills!!!!!!!!!!!!! How did I not realize it was that much? If I didn’t have credit card bills I would be rolling in it.

WTF!!!!!!!!!!!!!!!!!!!??????????????????????

Don’t get me wrong this whole situation is my fault and I understand that and am not making excuses. But I think there are some things inherently wrong with the way our society handles credit cards and what is ingrained into us at a very young age.

Not only do we have society telling me that we NEED all these different things, I grew up with a dad who bought what he wanted when he wanted and tried to buy some of our affection with things. Don’t get me wrong I love my dad and he was a great dad but no one is perfect and this was one of his faults.

I never knew that you couldn’t just go out and buy whatever you want, my mom was great and didn’t want us kids to worry about things so I never knew we were in debt or lived paycheck to paycheck or that my mom never bought things for herself because my dad was always overspending. I am kind of torn on whether I think that was 100% the correct approach or not, on the one hand I never worried about money and had a carefree childhood as children should but maybe it wouldn’t have taken me over a decade of digging myself a hole if I had been a little more aware of dads spending problems. IDK. Either way my mom is awesome so I lucked out there.

Society tells us from day one we need credit; want to rent an apartment? you need credit. want to buy a car? you need credit. want to buy a house? you need credit. It seems for everything in todays world you need credit, and what is the easiest way to get that, open a credit card the day you turn 18. And that is just about what I did, I turned 18 in April and by September I had my first shiny credit card with a $500 limit.

I kept my spending relatively in check and paid my minimum payment on time and after a little while that credit limit jumped up to $750. Woohoo!!!!! Still I couldn’t get into too much trouble with that amount, even maxed out the minimum monthly payment was $25.

Then the trouble started, my bank sent me a credit card with a $2,500 limit…….that is a little easier to get into trouble. It didn’t take me long to get both cards up near their limits, but I always paid the minimum amount required so all was well in the credit world. Apparently if you continually pay your bills on time they up your credit limit!!! Suddenly I look at my statement and I have a 4,900 credit limit! Sadly all I see is oh I have 2k available to me…….oooh that is a cute top I need that, oh I need Starbucks every day, oh Christmas presents for everyone! I feel like getting a massage and a facial, I am bummed out while living in the dorm and decide to go to 3 movies in a row and buy soda and food for each one to escape for the day. I’m gonna order a pizza and on and on and on it went. Both of those card have hovered within about 5% of their limit since a few months after I got each one.

Even that wasn’t too bad, between the two my minimum monthly payment totaled about $150.

Than about a year and a half ago I got beyond stupid. I had discovered my love for travel and thought I need a card with miles so I can get free airline tickets and use points for anything to do with travel, so I opened a 3rd credit card and the limit they gave me was stupid. And they had the “if you spend 3k in 3 months you get 60,000 bonus miles”, so I spent on anything and everything to hit that 3k and get those miles, and they did come in handy but I just kept spending and suddenly that card is maxed out and the monthly minimum payment is $300!!!!

I am in quite a bit of debt now and it is completely my own doing but I do think that maybe we should make people wait until they are older to get a credit card, until they are more responsible, or maybe limit the number of cards they can have until a certain time and definitely limit the amount of credit.

I also whole-heartedly think we need to teach kids budgeting and real life money management in high school. It has taken me over a decade to realize that I have a problem and need to change my thinking, but I am doing it and one day I will be out of debt.

About 2 months ago I cut up my first credit card!!!!!!!!!!!!! It will be paid off by the end of this year, big smiles!!!!!! Obviously it is that small one but every dollar counts! Cutting up that card felt wonderful and horrible all at the same time, I felt like cutting it up was wrong, like I would get in trouble for doing it. It was weird but I am so glad that I did, because as the balance goes down I cannot recharge on it and that is so important.

I am not perfect and I still have days where I want things I don’t need and days when I buy something I don’t need to or don’t have the money for. I am a work in progress but I am quite happy to say that progress is being made!!! And I am keeping an eagle’s eye watch on my credit score and the credit I have available on that card because seeing the progress helps.

I am so lucky to have a wonderful support system (MOM) who has helped me start taking these steps and start learning that I can still have things but it needs to be responsibly and in moderation.

If you have gotten yourself into the mess I have or feel like you might not have control over your spending, talk to someone. Don’t let it ruin your life.

Debtors Anonymous | Official Website

http://www.spenders.org/about.html

Check out the movie “Confessions of a Shopaholic” they overdramatize it but I can definitely relate to a few things in that movie. Plus it is adorable.

Thanks for reading my crazy long post.